Automotive Components

Print/Download Page As PDF

Invest in Lesotho’s

Automotive Sector

LESOTHO – The Precision-Labour Hub for Southern Africa’s Auto Cluster. Lesotho offers a cost-competitive, SACU-integrated base for OEMs, Tier‑2/3 automotive components and selective SKD/light assembly serving South African OEM hubs and growing AfCFTA markets.

Introduction

Lesotho offers a cost-competitive, SACU-integrated base for Tier‑2/3 automotive components and selective SKD/light assembly serving South African OEM hubs and growing AfCFTA markets. In 2025, the United States imposed sectoral tariffs on automobiles and specified auto parts under Section 232 measures that apply to South Africa and, by extension, SACU suppliers integrated into South Africa’s value chains. These developments heighten the case for regional localisation and supply-chain risk management under SAAM/APDP frameworks.

Lesotho Policy Priorities – Cluster and Supplier Development Lesotho’s policy stance is to consolidate and deepen a Tier‑2/3 supplier cluster anchored around the regionally established Tier‑1 investors (e.g. Adient) to support South African OEM pipelines. Priorities include: (i) localisation alignment with SAAM/APDP – qualifying cross‑border suppliers into South African programmes (local content, traceability, compliance) consistent with SAAM pillars on localisation, technology and skills, and market development; (ii) SACU trade‑facilitation for JIT/JIS – streamlining cross‑border movements on the Maseru–Gauteng, Eastern Cape Kwazulu Natal corridors and utilising marine port gateways for export; (iii) investment facilitation and aftercare via LNDC (serviced factory shells, permits facilitation, coordinated aftercare); (iv) skills, standards and quality systems – aligning TVET/upskilling and plant‑readiness with SAAM’s technology and skills pillar and OEM quality regimes; and (v) risk management in light of U.S. Section 232 – monitoring tariff developments that affect South Africa‑linked value chains and prioritising market diversification/regionalisation to reduce exposure to single trade lanes.

Strengths &

Opportunities

Lesotho is a member of the SACU and SADC and therefore enjoys duty and tariff-free access to the South African market. Customs clearance is relatively smooth and straightforward, and with Authorised Economic Operator (AEO) programme for firms, transporters and agents.

A GLOBAL MARKET OPPORTUNITY

The South African automotive industry supplies the SACU, SADC, EU and USA markets with vehicles, a market of around

The AfCFTA brings a new additional market base to all 54 African countries with a population of over 1.5 billion. The AfCFTA brings a new additional market base to all 54 African countries with a population of over 1.5bn.

INCREASED PRODUCTION

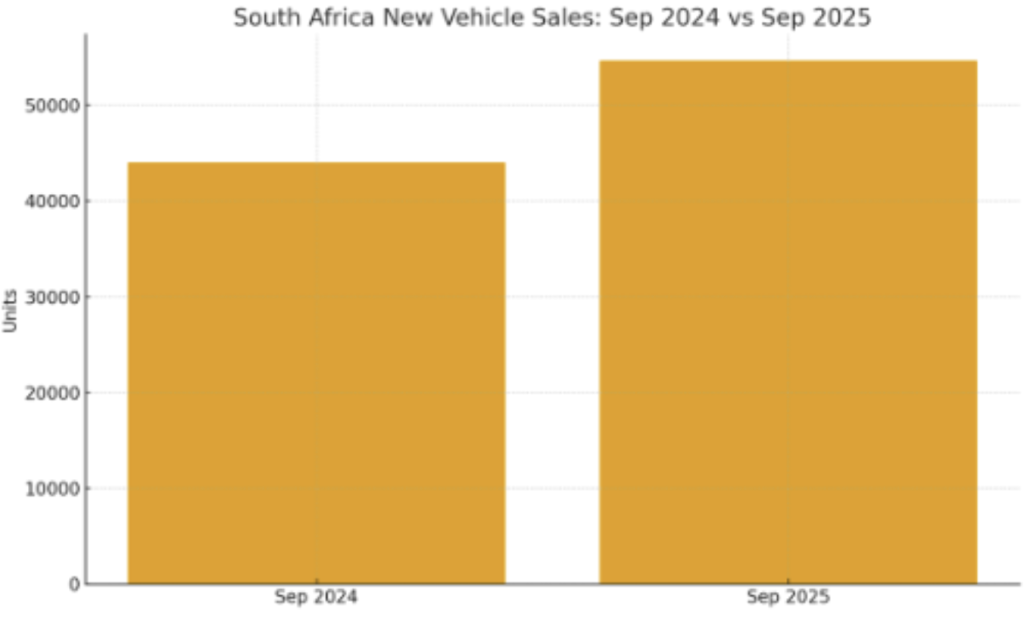

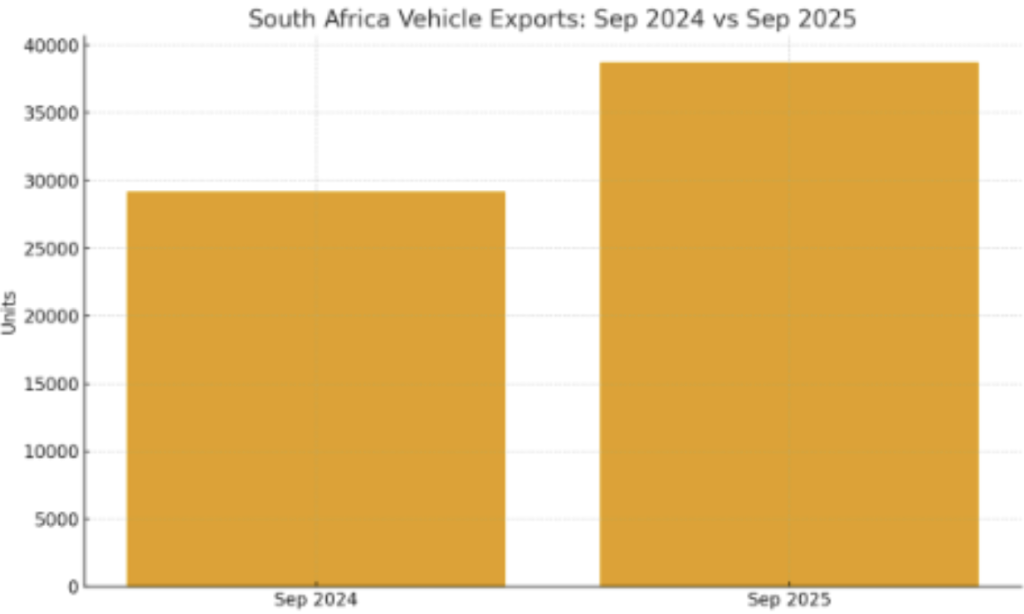

Despite tariff headwinds, South Africa’s domestic market strengthened: in September 2025, new-vehicle sales rose 24,3% to reach 54,700 units – the highest monthly level since 2015 – while vehicle exports rose 32.9% year-on-year to 38,772 units for the month. These dynamics sustain procurement demand across OEM clusters in Gauteng, KwaZulu-Natal and the Eastern Cape, where Lesotho-based suppliers can integrate via short-haul, just-in-time trucking routes and marine port gateways.

South Africa has eleven

automotive manufacturers:

Regional and Global integration and proximity to OEMs:

Duty-free movement within SACU and short-haul trucking enable just-in-time supply to South African assembly hubs; Maseru is 499 kms from Roslyn near Pretoria; 542 kms from Durban; and 702 kms from Port Elizabeth. Lesotho’s Tikoe (Maseru) and Belo (Butha-Buthe) industrial estates provide serviced factory shells suited to labour-intensive operations.

Policy alignment (SAAM/APDP):

South Africa’s Automotive Masterplan to 2035 and APDP sustain localisation and supplier-development levers that cross-border component makers can plug into via SA OEM contracts.

Export gateways:

Eastern Cape ports (Ngqura/Coega, Gqeberha, East London) function as the sector’s main export conduits with direct links into African markets, an outlet for Lesotho-made components and final products.

Incentives

Low corporate income tax: 10% on profits from manufacturing

Training:

Cost of Lesotho citizens allowable at 125% for tax purposes.

Withholding Tax:

• 10% on service contracts with non-residents.

• 25% on dividends distributed from income by resident companies to non-resident shareholders.

• No withholding tax on dividends distributed to Lesotho residents

VAT:

• 15% on goods and services sold in Lesotho

• 0% on direct exports Duty rebates and drawbacks under the SACU regime for specified materials/goods. Risk guarantees:

• Partial credit guarantee through the LNDC

• Facilitation support to identify and mobilize labour and skills development partnerships

Support from the LNDC includes:

• Serviced industrial and commercial sites at competitive rentals

• Provision of industrial and commercial

buildings at competitive rentals

• Financial assistance on a selective basis

• Investment facilitation services

• Assistance with permits and licenses

• Assistance with company registration

• Assistance with industrial relations issues

• Appraisal of investment projects

• Assistance with preparation of project briefs for the Environment Impact Assessment (EIA) Certification

Belo Industrial Park, Butha Buthe.

Automotive Component Factory, Maseru.

Tikoe Industrial Park, Maseru.

List of investment opportunities

Target Segments:

• Wire harnessing

• Seating / upholstery and foam sub-assemblies (interiors)

• Small plastics and light metal components (profiles, clips, retainers, moulded parts)

• Paneling

• Tooling and jig/fixture services: transmissions / tooling

• Selective SKD/light assembly for niche regional demand (subject to Rules-of-Origin and feasibility)

SDGs alignment

The project aligns with SDGs 1, 5, 8, 9, and 10.

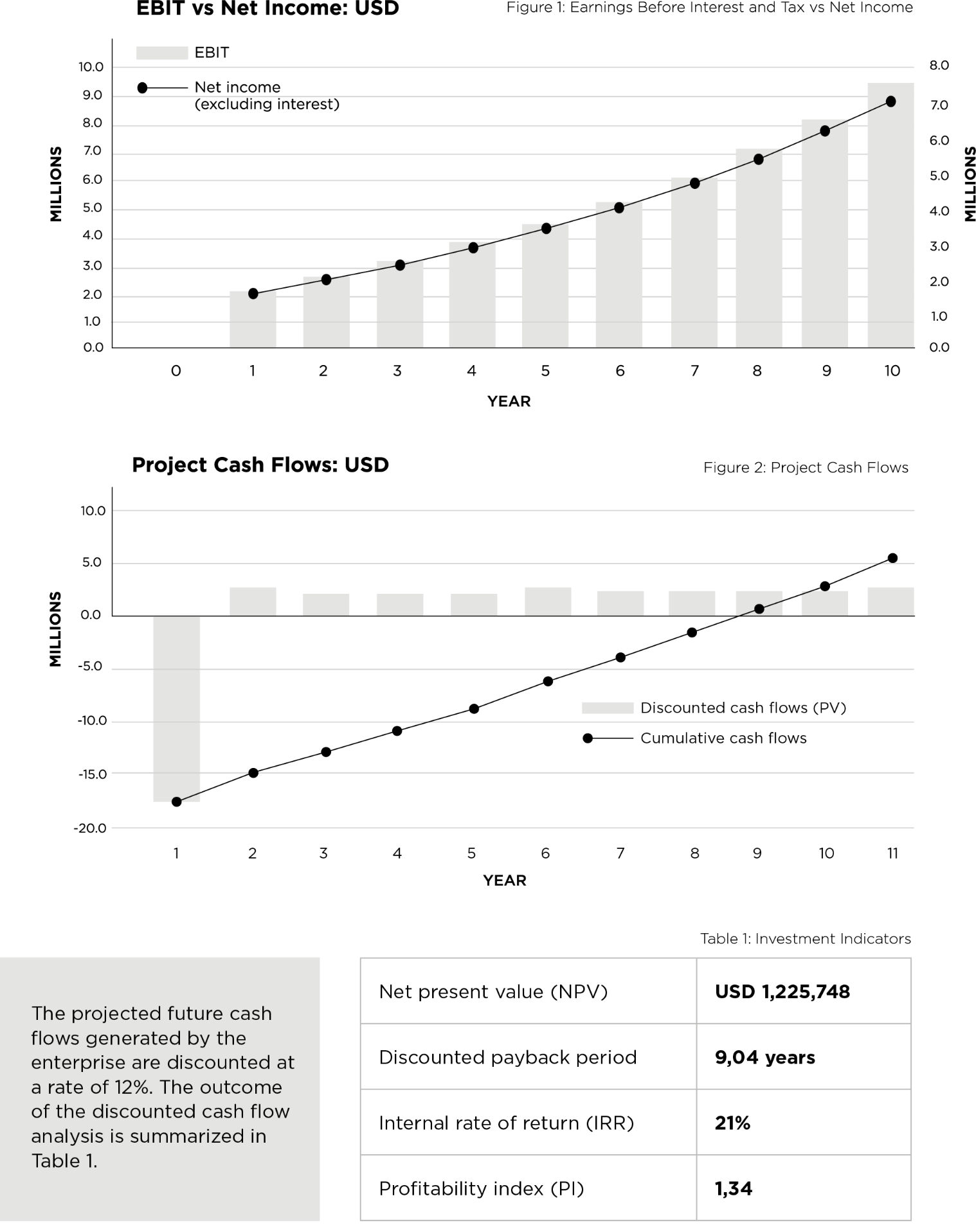

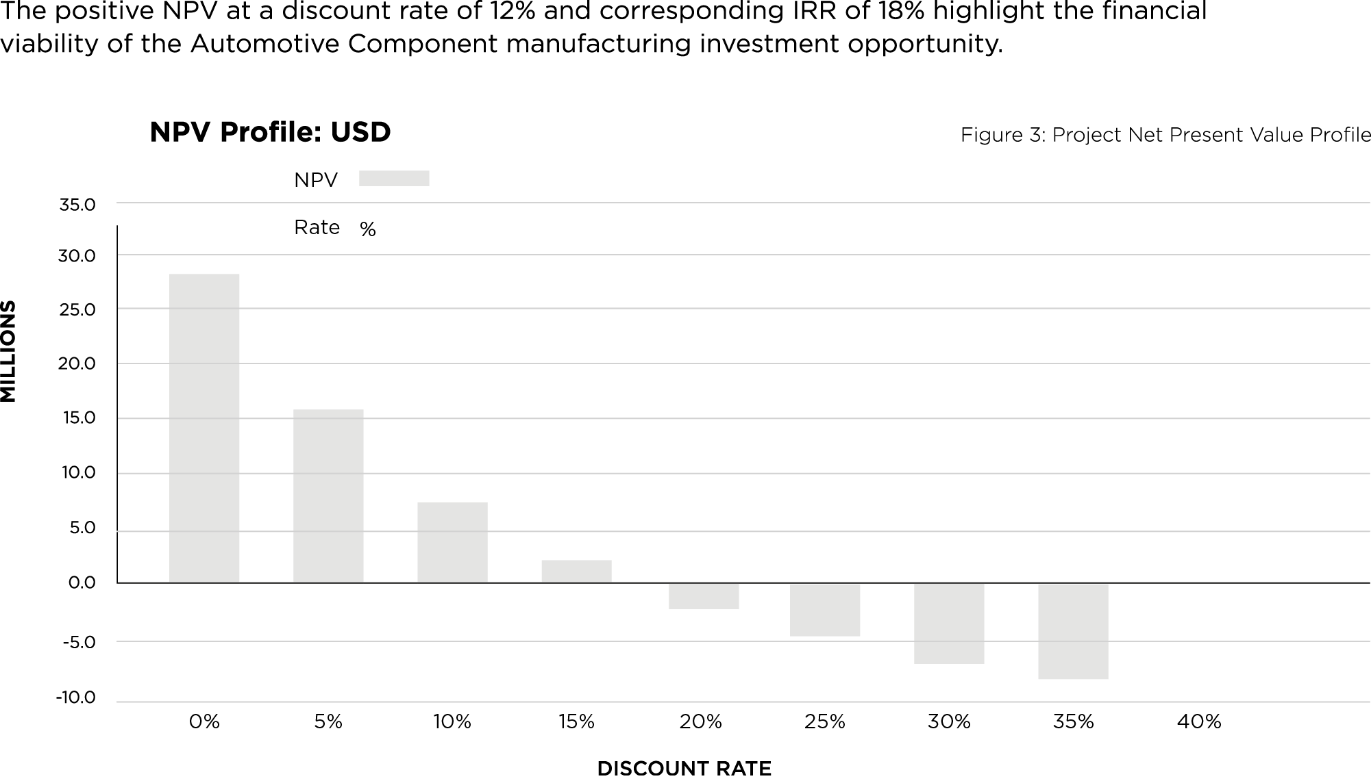

Financial Analysis

USD 17.5m

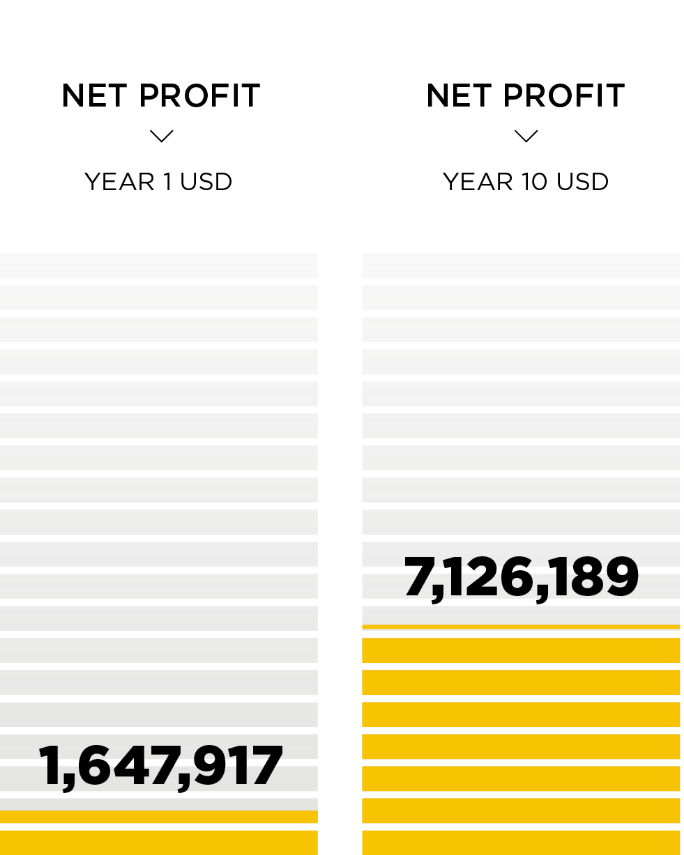

comprising fixed assets of USD 14.4m, pre-production expenditure of USD 555k and initial working capital of USD 2.5m will be required for the establishment of the Automotive Component manufacturing enterprise. The graphs below illustrate a financially viable operation with the opportunity expected to generate a profit throughout its operational life.

In addition to the positive NPV of and IRR, the initial investment cost of the project is expected to be fully recovered in under 9 years. The investment opportunity further responds favourably to Lesotho’s developmental objectives through its positive socio-economic impact in terms of employment creation, economic agglomeration and potential forex earning opportunities.

The enterprise’s annual net profit after tax increases from

The South African automotive industry supplies the SACU, SADC, EU and USA markets with vehicles, a market of around

USD 1.65m

USD 7.1m

in year 10.

Similarly, the projected cash flows of the envisaged project indicate that it will generate positive net cash flows throughout the 10-year operational period.

Financial Analysis

Automotive Component Factory, Maseru.

Belo Industrial Park, Butha Buthe.

This is a mid-sized automotive component manufacturing facility producing parts (e.g., plastic or metal components like bumpers or exhaust systems) for OEMs. The plant has a production capacity of 50,000 units annually. The financial analysis of the Automotive Components investment opportunity is computed over a ten-year period. Revenue and expenditure projections are in line with industry growth prospects and market potential and have been informed by and benchmarked against industry standards and norms. In addition, assumptions relating to inflation: depreciation and salvage value: and company tax have been worked out based on the existing laws and directives of the country. The figures above represent high level estimates as of October 2025 and are not derived from a full feasibility study. Investors are advised to conduct their own due diligence. The project assumes that the investor will have a viable business case that is driven by international client demand.

DISCLAIMER

This web page provides a strategic overview. All financial figures are based on a high-level investment opportunity model and should be used as an indicator of potential only. Investors are strongly encouraged to conduct independent due diligence and a full feasibility study with the support of the LNDC to validate all assumptions under current market conditions.